Overseas Transaction Fees – Credit Cards

In the context of Singapore. Updated 25 January 2017.

What payment methods should you use for overseas booking and travel? PayPal or Credit Card? Visa, MasterCard or Amex? Which bank? Before I go on to the different banks’ overseas transaction fees for credit cards, I have a word to say about PayPal.

Many people had said that the currency conversion fee for Paypal is typically higher than banks/credit card companies. I tried to confirm it with the PayPal website – but instead found a non-transparent fee structure here: A currency conversion (admin) fee may apply and be included in the exchange rate before adding it to the purchase amount. So I decided it’s to go with the general sentiment and not use PayPal.

Credit Card – Overseas Activation

Important:

- Activate your credit and ATM cards for overseas use and cash withdrawals.

- Credit Card Activation links: UOB, Citibank, Standard Chartered, DBS iBanking or ATMs, OCBC, Bank of China (online banking)

- ATM Card Activation links can be found here.

After I looked through a few (not all) banks’ user agreements, I came to a few conclusions for overseas credit card fees (without regards to the card reward program):

- Use Visa/MasterCard and not Amex.

- For AUD transactions, UOB cards will be good, since you only have to bear the exchange risk once.

- Many credit cards offer rebates on overseas transactions now. But make sure you read the fine print.

Overseas Transactions – Dynamic Currency Conversion or not?

There are many charges to your credit card transaction. So cash is still king, where you don’t have the admin and conversion fee, but lose/gain only at the exchange rate. However, credit card is still good in case you run out of cash overseas. Just so you know, there are two types of currency conversion for debit/credit cards. Firstly there’s the normal overseas transaction paying in foreign currency and then the dynamic currency conversion (“DCC”).

Depending on the conversion method and bank you choose, you are charged one of three ways:

- Foreign transaction fees

- Dynamic currency conversion fees

- Dynamic currency conversion fees + foreign transaction fees (came across this for OCBC, enlighten me if you know of other banks)

In my following explanation, it’s assuming your credit card’s home currency is Singapore Dollars (SGD).

1) Foreign Transaction (non-DCC)

a) Firstly, the foreign amount is converted to SGD with prevailing exchange rate:

- Transaction in US dollars = Converted to Singapore dollars.

- Transactions in other currencies = Converted first to US dollars and then to Singapore dollars.

- Exceptions:

- UOB: Converts US dollars and Australian dollars directly to Singapore dollars.

- UnionPay Debit Card: Transactions in US Dollar, Chinese Yuan (CNY) and Brunei Dollar (BND) dollars convert directly to Singapore dollars.

The exchange rate is usually determined by Visa, MasterCard or AMEX, or in some cases by the bank. Note that this double currency conversion usually means extra costs, though negligible with smaller transactions. Moreover, the prevailing exchange rate for your foreign transaction amount is applied on the date of posting to the Card Account and may be different from the rate that’s on the date of transaction.

b) Other than exchange rate difference, you pay for a foreign transaction fee which comprises of:

- Bank administrative fee

- Conversion costs charged by Visa, MasterCard, AMEX, etc.

Credit: mmmsimpsons.tumblr.com

2) Dynamic currency conversion (“DCC”)

Dynamic currency conversion is a service offered at selected overseas ATMs, websites or by certain merchants. This is also known as Singapore Dollar Transactions processed Overseas.

Situations when you are using DCC service, including but not limited to these:

- Retail: Choose to pay in your home currency (SGD) rather than the local currency of the place your are at. For example, a Hong Kong merchant’s cashier ask if you want to pay in HK$553 or S$100. If you choose to pay in S$100, you are effecting DCC.

- Online: Charge your Visa and MasterCard cards in Singapore Dollars on overseas based websites or Singapore websites that processed payments overseas.

Should you use DCC when you shop overseas or online?

As you may see in the charges below, DCC is lower than foreign transaction fee charged. However, many online sources recommend NOT to use DCC because of the non-transparent fee structure. There may be unseen markups computed within the transaction amount.

Additionally, the exchange rate applied will be determined by the relevant merchant or DCC service provider, which is generally less favorable than your credit card bank. The merchant’s rate can be 3 to 8% higher. Also, you might not be eligible for some credit card rewards which requires you to transact in foreign currencies.

As far as I know, only VISA and MasterCard charge for DCC. Other than the undisclosed marked up exchange rate, you are charged a DCC fee:

- Up to 1% on all converted amounts for any Visa and MasterCard transaction presented in foreign currency that you choose to pay in Singapore dollars via DCC. (See below for details regarding various banks).

- Up to 1.8% bank admin charges for debit cards.

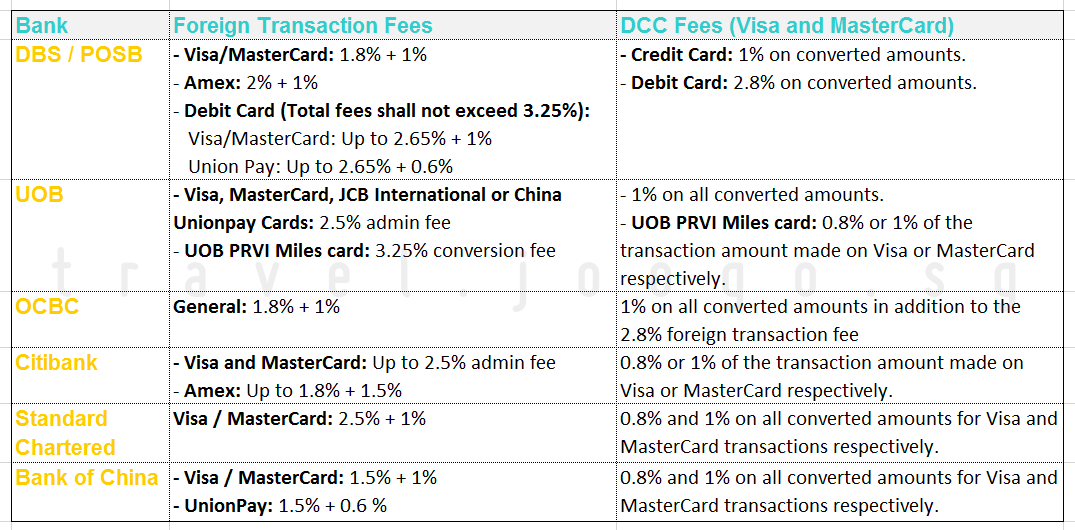

Overseas Transaction Fees – Banks and Credit Cards

Overseas Transaction Fee* = Bank Admin Fee + Conversion Fee + Exchange Rate^

DCC Fee Structure = DCC Fee + Exchange Rate^

*% on converted amounts, unless otherwise stated

^ not stated in the following

As mentioned, depending on the conversion method and bank you choose, you are charged one of three ways:

- Foreign transaction fees

- Dynamic currency conversion fees

- Dynamic currency conversion fees + foreign transaction fees (came across this for OCBC)

Notes:

- If you are going Japan, consider using JCB. I’ve enjoyed JCB perks over there using UOB JCB card.

- If you are going to China, you might want to consider using a UnionPay cards. For e.g. BOC UnionPay Dual Currency Debit Card, there’s no currency exchange fees for all RMB transactions through RMB account (just make sure you have sufficient balance inside). Other than Bank of China, other banks like DBS and UOB has UnionPay cards too.

References:

- www.dbs.com.sg/personal/cards/cards-rates-fees.page

- www.uob.com.sg/personal/cards/credit/tnc.html (Appendix 1)

http://uob.com.sg/assets/pdfs/cards/Terms_and_Conditions_Governing_UOB_PRVI_Miles_Card.pdf - www.ocbc.com/personal-banking/Help-and-Support/Credit-Cards.html

- www.citibank.com.sg/gcb/static/banking_fees.htm

- www.sc.com/sg/assets/pws/pdf/latest_credit_card_terms.pdf

- www.bankofchina.com/sg/bocinfo/bi4/201001/t20100120_955877.html

Phew that’s a lot of numbers and information! Hope you are able to decide which bank/card is best for you. You can also refer to my next post for overseas ATM withdrawal charges. :)

Thanks, this is really helpful comparison. looks VISA from DBS or BOC has the best rate without DCC.

Hi, does this mean that if I want to shop on Amazon using an OCBC credit card… i am better off paying in USD (instead of SGD)? Thanks!

Hello Wong,

Yes, that’s right for OCBC. I’ve updated the post to clarify on the dynamic currency conversion (paying SGD for foreign transactions). The DCC charge for OCBC seems to be in addition to their foreign transaction fee.

Also, Amazon might charge you at a much higher exchange rate than if you have gone through the bank. However, for Amazon, you can check its exchange rate and charges to see if you can accept them (https://www.amazon.com/gp/help/customer/display.html/ref=hp_left_v4_sib?ie=UTF8&nodeId=201895450).

Hope this helps!

Yes, this definitely helps! Thanks so much Christina :)

The other thing I was wondering about also is this thing called RateX (https://www.ratex.co/). Do you think RateX is considered a form of “dynamic currency conversion”, meaning it would still be cheaper to buy from Amazon in USD, rather than in SGD via RateX?

I have written in to RateX to enquire about whether they are a form of “dynamic currency conversion” but they don’t seem to be replying…

Appreciate any inputs you may have on this! THANKS AGAIN!!! :)

Great! From what I understand from their website (FAQ), the USD retail prices are converted at an exchange rate you can find online. So you simply pay SGD after the conversion without any other transaction fees. It sounds like a good deal, but judging from their non-reply, you might want to re-consider using them. Since when it comes to money matters, you might need a fast response time. :)

Thanks again for your response Christina! :D

Despite the non-reply I just went ahead and made my purchase via RateX. Seems ok. Will update if anything bad happens. If not, yes the deal is probably as good as it sounds!

I am planning to visit USA and will use an SG credit card.

Is it better to use a Visa, Master or Amex card? Which of them will be charging a lower fee.

Hello Freddy, it depends on the bank and type of card you are carrying, but generally amex charges a higher rate.

Hi Christina,

Do you know if charges in JPY on the UOB JCB card is converted to USD first then to SGD or converted to SGD direct?

According to their card agreement, “The transaction will be converted at the prevailing exchange rates of the relevant credit card company, first to USD then, to SGD.” :)

Hi Christina,

If I have credit cards from the 3 local banks, Citibank actually provides the best rate for foreign transaction fee. Is that right?

I mean in addition to the local banks, I also have Citibank card.

Based on their T&C, you are right. UOB should be quite on par too.

Hey Christina,

I need a card mainly for travels like low atm withdrawals fees internationally, overseas online purchases, airline bookings; also another card for basic spending locally. If possible both cards has low min spending requirement. What options do i have? Cheers

Hello Ash, sorry for the late reply. Usually I go with Citibank ATM card because their ATMs are available more widely overseas and has no additional admin charge. While for the card locally, there are many options – depending if you prefer cash back , miles, etc. I don’t think I am the best person to ask – you probably can find blogs who do detailed review of credit cards. Cheers!